Trending Now

- 1KOSPI

8

- 2Hollywood

8

- 3KOSDAQ

7

- 4shutdown

-2

- 5Bitcoin

-1

- 6ETF

4

- 7Mastercard

3

- 8dollar

2

- 9Ethereum

1

- 10stablecoin

America is a blessed nation. It has vast land, a large population, and abundant resources. Top universities across the United States attract the world's finest talent each year, generating more knowledge, technology, and wealth. However, among America's many strengths, its most powerful weapon—what truly makes America what it is—lies in the fact that its currency, the dollar, serves as the world's reserve currency.

The greatest export from the world's superpower America is neither automobiles, weapons, nor AI. America's most powerful weapon and export is the dollar—a currency that maintains demand regardless of how much is printed.

"He who would be king must bear the weight of the crown." Becoming the issuer of a reserve currency grants a nation the power to influence the global economy through its own monetary policy, but this also entails significant responsibility. Let's examine what conditions are necessary for a currency to become a reserve currency, what kind of country should issue a reserve currency, and what dilemmas reserve currency nations face.

Definitions of a reserve currency vary among economists. However, there's no need to overcomplicate it. A reserve currency (world currency) simply means the most universally used currency in the world. A reserve currency serves as the base currency for international trade and financial transactions.

The Amsterdam Exchange Bank, which served as the center of global finance in the 17th century, significantly contributed to establishing the Dutch guilder as a reserve currency. (Source: WGA)

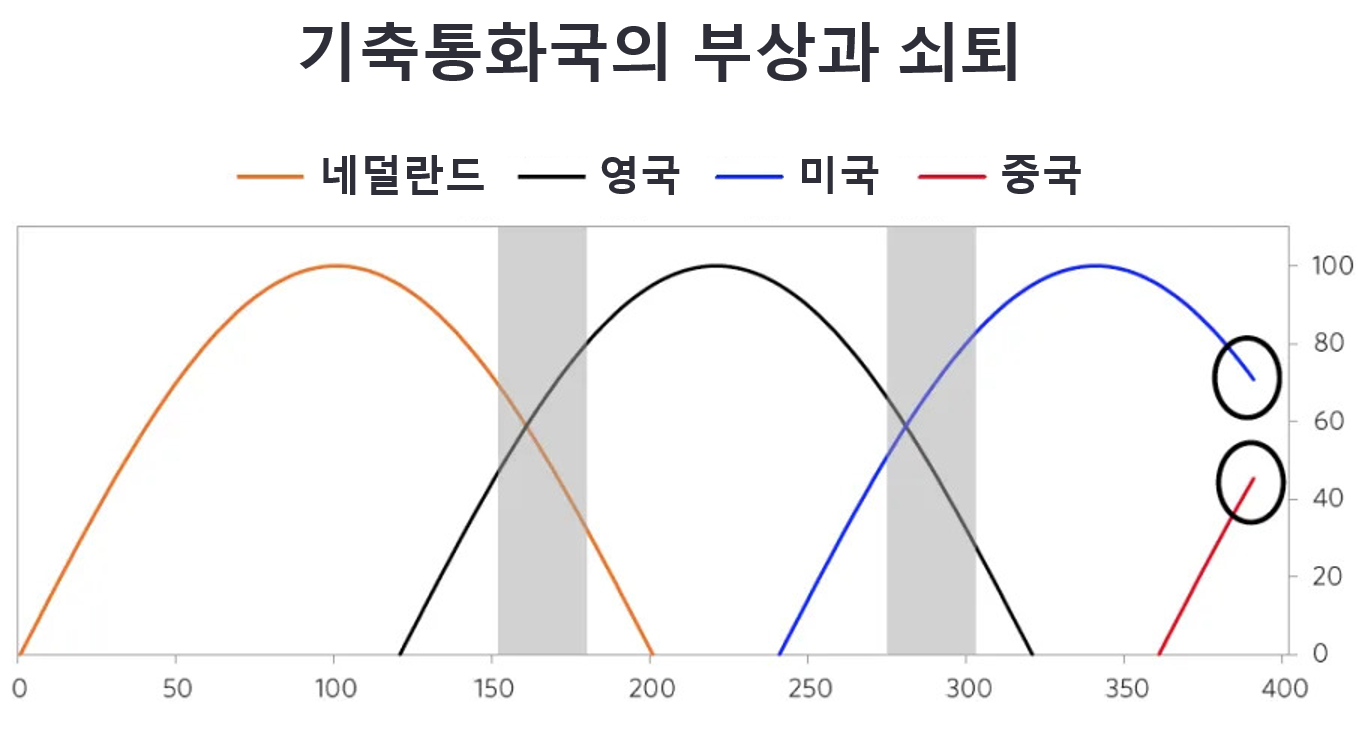

Historically, reserve currencies have changed. Even since the formation of the modern financial order, the Dutch guilder functioned as the reserve currency in the 17th century, but completely lost its status as the reserve currency after the Fourth Anglo-Dutch War in 1784. The British pound subsequently became the reserve currency and served as such until after World War II.

As we examined in Chapter 1, "The History and Evolution of Money," the U.S. dollar became the world's reserve currency through the 1944 Bretton Woods Agreement and has maintained that status to this day. The dollar is used as the primary currency for international trade, financial transactions, investments, and foreign exchange reserves, with most commodity transactions, including oil, settled in dollars. The dollar accounts for approximately 44% of global trade settlement currency and 60% of central bank foreign exchange reserves worldwide.

While economists differ in their interpretations and emphasis, there are generally four main conditions for a reserve currency. These are: sufficient liquidity, value stability, credibility, and the absence of alternative currencies. Let's examine what conditions are necessary for a currency to function as the world's reserve currency.

First, a reserve currency must provide sufficient liquidity for countries around the world to use in trade, financial transactions, and foreign exchange reserves. This means having enough currency to meet all transaction demands in the global economy. It must serve as a payment method in international trade and financial transactions, function as a medium of exchange in the foreign exchange market, and be held as foreign exchange reserves by countries to secure the value of their own currencies. Some countries even abandon their own currencies and use the U.S. dollar instead.

Providing sufficient liquidity is both a duty of the reserve currency nation and an essential condition for maintaining its reserve currency status. The fact that silver coins could be used as a global common currency in the past was because Spain could supply an enormous amount of silver coins through the development of the Potosí silver mines. Without such circulation volume, silver coins would have only functioned as currency within specific countries or regions.

Second, a reserve currency must guarantee value stability. Consider a reserve currency's key function as a target for foreign exchange reserves. South Korea's dollar foreign exchange reserves stand at $415.6 billion as of 2024. If the value of the U.S. dollar were to fluctuate easily, countries around the world holding dollars as foreign exchange reserves could lose tens or hundreds of trillions in national wealth overnight. In such a scenario, that currency would no longer be chosen as a target currency for foreign exchange reserves in the global economy.

Historically, reserve currency nations have sometimes guaranteed the value of their currencies through overwhelming gold reserves. In the early 20th century, following World War I, the United States accumulated vast amounts of gold through European countries' war debt repayments and post-war reconstruction, allowing it to implement the gold standard and maintain the dollar's value stability.

Third, a reserve currency must have credibility. The credibility of a reserve currency stems from confidence in the nation that issues it. This originates from three main factors: overwhelming superiority in military power and diplomatic influence, advanced financial markets and financial systems, and high national credit ratings. These factors work together to form international trust in the currency and its issuing country.

Fourth, a reserve currency necessarily requires the absence of viable alternative currencies. If a competing nation emerges that garners more trust than the existing reserve currency nation, the reserve currency will be threatened, and the world order may change through hegemonic struggles or wars. Conversely, if no nation emerges to challenge the military, political, and financial hegemony of the reserve currency nation, it can extend its status.

According to Ray Dalio, the rise and fall of hegemonic powers follow cycles, and since the establishment of the modern financial order in the 17th century, the fate of reserve currency nations has followed the same pattern. (Source: economicprinciples.org)

While becoming a reserve currency nation grants enormous privileges, it also brings significant burdens. This is known as the "Triffin Dilemma," which refers to the paradoxical situation where the reserve currency nation must increase its debt and run trade deficits to supply sufficient liquidity.

During the past 80 years when the United States was the reserve currency nation, the growing global economy required more dollar liquidity, and to provide this, the U.S. had to continually run trade deficits. However, continued deficits can devalue the dollar, undermining its credibility as a reserve currency. Conversely, if the U.S. tries to reduce trade deficits, it cannot supply enough dollars to the global economy, which would contract the world economy and lead countries to seek alternative currencies.

Trump declared at his inauguration ceremony held at the U.S. Capitol Rotunda on January 20 that "America's golden age is about to begin." However, the problems awaiting him in America are by no means easy. In fact, they are more serious and urgent than ever before. The problems facing the United States now are a combination of complex and paradoxical issues where solving one tangle creates another.

The primary duty of a U.S. president is to maintain the dollar's status as the reserve currency. If the dollar ceases to be the reserve currency, the United States can no longer be called the world's hegemonic power. The U.S. president must maintain the dollar's reserve currency status by whatever means necessary, above all other tasks.

In particular, as the reserve currency nation, the United States must be able to continuously supply liquidity. It must continue to provide liquidity without problems as the central currency for increasing global trade and financial transactions. To continue providing liquidity to the global economy, it must accept trade deficits and issue debt.

But the reason for maintaining reserve currency status is ultimately for the nation's own interests. This is even more so for Trump, who has proclaimed "America First." Trump won with the support of the Rust Belt in the northeast, which has declined due to the deterioration of U.S. manufacturing, so he has shown strong will to revitalize manufacturing through reshoring and tariffs, and to resolve trade deficits. In that case, he would aim for a trade surplus, which means dollars would flow in rather than circulate out. This is when he faces the Triffin Dilemma as a reserve currency nation that must circulate currency to the global economy.

The Trump administration must use all financial, economic, and political means to solve the Triffin Dilemma and maintain the appropriate value of the dollar. The dollar must be somewhat strong to maintain its status as a reserve currency. However, if it's too strong, the price of U.S. products rises and manufacturing competitiveness declines. This deepens the trade deficit and fails to achieve the revitalization of manufacturing that Trump sought. But if the dollar weakens, it becomes difficult to maintain its value as a reserve currency. Trump 2.0 must devise an unprecedented strategy to maintain the appropriate value of the dollar.

In the 1990s, the US sacrificed manufacturing to maintain its reserve currency status. Trump, however, aims to secure both manufacturing strength and dollar dominance simultaneously. (Source: MIT Press)

The United States now faces another complex and paradoxical challenge: reducing debt while securing funding. President Trump must manage and reduce the national debt that grew exponentially under the Biden administration while also raising funds to pursue his promised policies. This problem isn't something that can be solved solely at the monetary policy level but includes complex elements closely linked to fiscal policy.

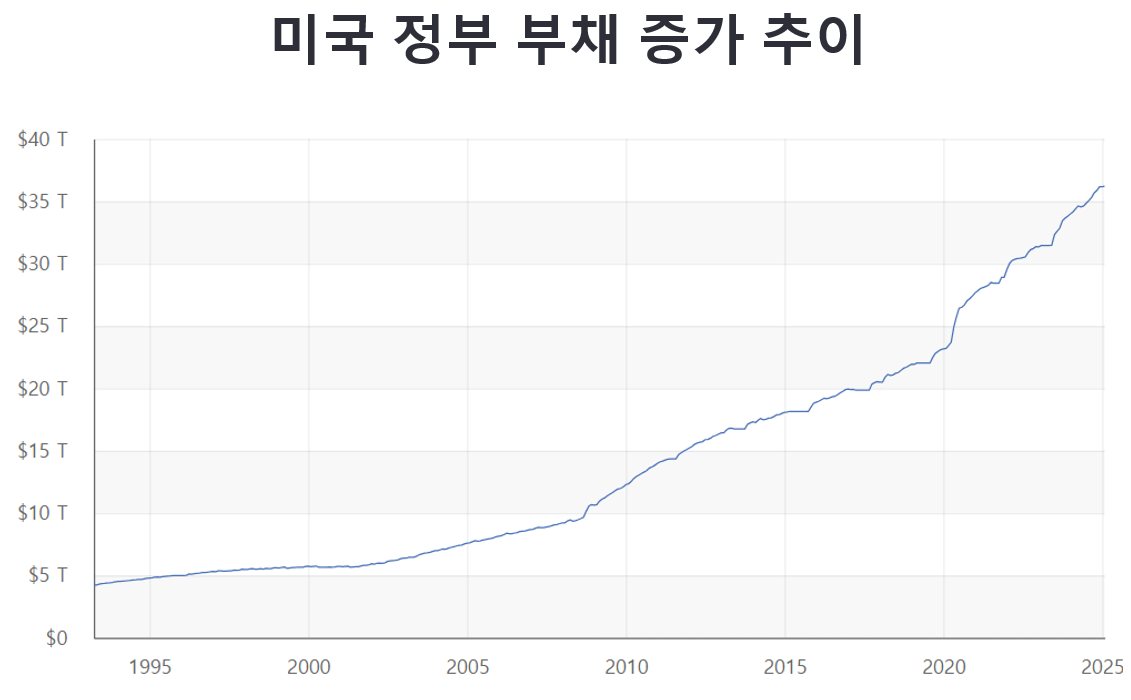

The current U.S. debt situation is very serious. The national debt exceeded $36 trillion in early 2025, with about $12 trillion in federal debt accumulated since 2020 alone. This deficit spending approaches levels seen during World War II in terms of GDP ratio, and markets express high concern about the U.S.'s continued deficit fiscal operations.

US government debt exceeded $36 trillion as of January 2025, with debt doubling approximately every decade. (Source: U.S. Treasury)

Looking at the growth trend of M2 money supply, which measures the amount of currency circulating in an economy, an enormous amount of liquidity was supplied after COVID, leading to inflation and dollar value depreciation. Regarding this, Ray Dalio, author of "Changing World Order," pointed out that too much "debt monetization" is occurring in the United States.

Debt monetization refers to the policy of central banks printing money to directly purchase government bonds, which can alleviate fiscal difficulties in the short term but leads to inflation and reduced currency credibility in the long term. The dollar is already in a sufficiently dangerous situation, and if bond issuance continues not only in monetary policy but also in fiscal policy, the dollar's value as a reserve currency could further deteriorate.

The instability of the U.S. financial system surfaced during the Silicon Valley Bank (SVB) collapse in 2023. As inflation surged due to liquidity released during the COVID period, the Fed rapidly raised interest rates, causing bond prices to fall. This also reduced the value of bonds held by regional banks, leading to SVB's bankruptcy. Such accumulated trust issues in the U.S. financial system could reach a point where doubt about the dollar suddenly explodes.

When the crisis emerged, SVB customers withdrew approximately $42 billion in a single day. The Biden administration ultimately decided to fully guarantee SVB customers' deposits. (Source: Reuters)

Some argue that the United States, as a reserve currency nation, doesn't need to resolve its debt, but this isn't realistic. No individual, organization, or nation can avoid addressing its debt. Even if it's unavoidable profligacy, the end of profligacy leads only to catastrophe. The U.S. economic system could collapse if debt isn't controlled.

Yet President Trump must inevitably continue to raise funds to realize his second-term promises. He must reduce and manage debt but simultaneously must increase debt. Previous administrations sacrificed the nation's long-term fiscal health to borrow for short-term goals. But now the United States, and President Trump, have reached a point where they can no longer choose between short-term and long-term national interests.

Nevertheless, Trump's second term must manage debt while securing funds for short-term economic growth and reform. Until now, the U.S. has raised funds by issuing Treasury bonds, considered the world's safest assets. However, as China continuously reduces its U.S. Treasury holdings, the U.S. finds itself needing to find new demand for its bonds. Trump needs the ultimate solution—one that can reduce debt while continuing to issue bonds.

Since 1944, when the dollar became the world's reserve currency, the United States has faced serious challenges multiple times. Each time a crisis threatened the dollar's reserve currency status—whether from fiscal deficits due to the Vietnam War, global economic turmoil from oil shocks, the economic rise of Japan and Germany, or the 2008 financial crisis—the U.S. overcame it through new strategies and actually strengthened the dollar's position. The dollar has adapted to changing times, evolving from the gold standard to the petrodollar and then to financial hegemony.

Having returned to the White House, Trump faces unprecedented challenges. A $36 trillion national debt, trade deficits, China's rise, and de-dollarization movements combine to threaten the dollar system with complex and paradoxical problems. Trump's solution appears to be a "Dollar 4.0" system.

World War II fundamentally reshaped the global economic order. While major European countries suffered economic damage from the war, the United States accumulated enormous gold through war-related economic benefits. In 1944, the U.S. held 75% of the world's gold reserves, about 20,000 tons. This overwhelming gold reserve provided a powerful foundation supporting the dollar's value.

Under the Bretton Woods system, the United States promised to maintain a fixed exchange rate of $35 per ounce of gold. Other countries' currencies were fixed to the dollar, and central banks could exchange their dollars for gold at any time. This "dollar-gold convertibility" promise brought absolute trust in the dollar. The world recognized the dollar as an asset "as safe as gold," which became a decisive opportunity for the dollar to establish itself as the de facto reserve currency. From 1944 to 1971, under the Bretton Woods system, the dollar's value remained remarkably stable, and this period is often called the "golden age of capitalism."

In the late 1960s, the first major crisis for the dollar system came as Vietnam War costs surged. To fund the war, the U.S. excessively issued dollars, threatening the dollar's value. French President de Gaulle notably declared he would exchange all France's dollars for gold. As other countries showed signs of following suit, on August 15, 1971, President Nixon took the dramatic step of ending dollar-gold convertibility in what became known as the "Nixon Shock."

However, the U.S. soon found a new solution. In 1974, Secretary of State Kissinger reached a historic agreement with Saudi Arabia. Saudi Arabia would settle oil trades exclusively in dollars, and the U.S. would guarantee Saudi security. Other OPEC members soon joined this system, marking the beginning of the "petrodollar system." Now dollars were needed to buy and sell oil, creating global demand for dollars. With oil replacing gold as a new value base, the dollar became an even more powerful reserve currency than before.

Entering the 1980s, the United States faced a new challenge: massive trade deficits, particularly severe trade imbalances with Japan and Germany. This was an inevitable dilemma facing the reserve currency nation. For the world economy to grow, more dollars needed to be supplied, inevitably leading to U.S. trade deficits—the so-called "Triffin Dilemma."

The Reagan administration solved this problem in a very unique way. In September 1985, at a G5 meeting at the Plaza Hotel, they negotiated an agreement to significantly appreciate the Japanese yen and German mark. Over the next two years, the yen's value more than doubled, and the German mark also appreciated significantly. This was a clever method to resolve trade imbalances with specific countries without a general weakening of the dollar.

But this policy also hit limits. Japan and Germany's competitiveness remained strong. In response, in 1995, the U.S. pushed for a complete strategy reversal with the "Reverse Plaza Accord." They decided to no longer compete in manufacturing but instead foster the financial industry. They accepted dollar strength to attract global capital to Wall Street. This ultimately proved enormously successful. The U.S. became the center of global finance, and the capital accumulated there supported Silicon Valley's growth, forming the foundation for U.S. IT industry development.

Trump appeared on The Oprah Winfrey Show in 1988, stating that the U.S. needed to address trade imbalances with other countries and that he would take action if nobody else does. One certainty about Trump is that he has no intention of circumventing the Triffin dilemma. (Source: OWN)

Now Trump is preparing an innovative masterstroke to overcome the dollar crisis accumulated over the past 80 years. This strategy, called "Dollar 4.0," is based on two pillars: stablecoins and Bitcoin reserves. This isn't a simple policy change but aims to build a new dollar hegemony suited to the digital age.

The first pillar is providing new dollar liquidity through stablecoins. Trump opposes CBDC adoption, instead actively fostering private stablecoins. This has several strategic implications.

First, stablecoins can become a new source of Treasury bond demand. Stablecoin issuers must hold U.S. Treasury bonds as reserves to guarantee the value of their issued coins. In a situation where China is reducing its U.S. Treasury holdings, this is very significant. As of 2024, major stablecoin issuers held over $100 billion in U.S. Treasury bonds, and this amount is expected to grow as the market expands.

Additionally, stablecoins can be a new circulation channel for the reserve currency dollar. As the cryptocurrency market grows and stablecoin issuance and usage increase, this becomes a means to supply new liquidity as a reserve currency. In particular, it can be a new solution to the Triffin Dilemma, where the U.S. must supply dollar liquidity to the world economy while pursuing trade surpluses.

The second pillar is solving the debt problem through Bitcoin strategic reserves. The "Bitcoin Strategic Reserve" policy, proposed by Senator Cynthia Lummis and being prepared for implementation by Trump, has the core objective of addressing the United States' $36 trillion national debt.

Using Bitcoin reserves to pay off a nation's debt may sound unrealistic. But Ray Dalio explains in his book "Changing World Order" that such behavior has historically been repeated:

"Printing too much non-convertible money leads to the selling of debt assets and the 'bank runs' described earlier. As a result, the value of money and credit falls, and people try to get rid of the currency and debt to move into something else... The big blowout (large-scale debt default or currency devaluation) happens about once every 50 to 75 years."

"This practice of accumulating debt and then writing it off all at once has persisted for thousands of years and was even institutionalized. The Old Testament contains passages about the Year of Jubilee, which happened every 50 years and was when debts were forgiven. Because the debt cycle comes along about once every 50 years, people prepared for it and acted accordingly."

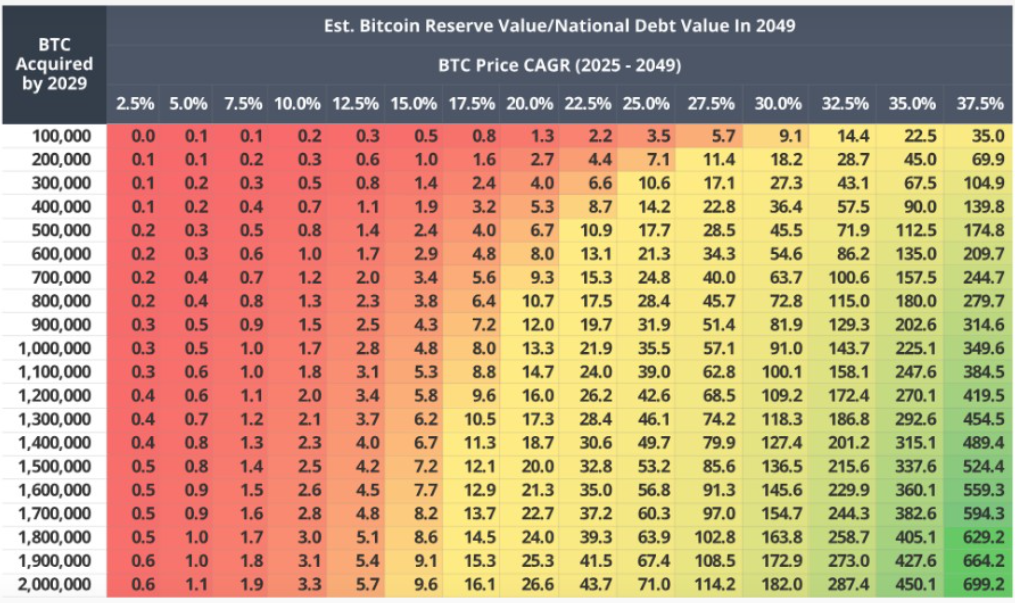

According to analysis by asset management firm VanEck, if the United States creates a reserve of 1 million Bitcoins as proposed by Senator Cynthia Lummis, it could reduce the national debt by 35% over the next 24 years. This is based on the projection that Bitcoin prices will rise to $42.3 million by 2049, assuming a compound annual growth rate (CAGR) of 25%. During the same period, the U.S. national debt is expected to increase by an average of 5% annually to reach $119.3 trillion, of which about $42 trillion could be offset by Bitcoin reserves.

VanEck's projection assumes Bitcoin will rise 423-fold over the next 25 years to account for about 18% of global financial assets. Even this aggressive assumption would only solve 35% of the total debt. (Source: VanEck)

The Dollar 4.0 strategy is an extension of how the United States has historically responded to dollar crises. If Dollar 1.0, which began with the 1944 Bretton Woods system, built dollar credibility through the gold standard, Dollar 2.0 after the 1971 Nixon Shock established dollar indispensability through the petrodollar system. Dollar 3.0, beginning with the 1985 Plaza Accord, maintained the dollar's status through global financial hegemony.

Now Trump is attempting the fourth evolution of the dollar system through new tools: stablecoins and Bitcoin. This is an attempt to build a new form of dollar hegemony suited to the digital age, and simultaneously an innovative solution to the debt problem and Triffin Dilemma facing the United States.

However, the conundrums facing the United States as a reserve currency nation are so complex and paradoxical that they may require solutions more complex and creative than the combination of stablecoins and Bitcoin reserves. When transitioning from Dollar 1.0 to 2.0, and from 2.0 to 3.0, only one or two key problems needed to be solved or bypassed. But now multiple complex issues must be solved simultaneously.

The emergence and growth of stablecoins clearly offer a breakthrough for many problems facing the United States. With the growth of the cryptocurrency industry, stablecoins have become a new source of demand for U.S. Treasury bonds and are expected to continue growing. They are also expected to supply the reserve currency dollar to the global trade market in a different form.

However, a clear limitation of stablecoins is that as they grow and become more widely used, the amount of Treasury bond issuance by the U.S. Treasury must proportionally increase. Currently, of the approximately $36 trillion U.S. debt, about $28 trillion—nearly 80%—are bonds. The continued increase in bond issuance will only worsen the debt problem, which is the biggest issue the United States faces as a reserve currency nation.

The approach of strategically stockpiling Bitcoin to solve America's debt problem is indeed a strategy that could extend U.S. hegemony by decades if actually realized. VanEck's analysis suggesting it could resolve 35% of the national debt over 24 years is certainly an attractive scenario.

But let's consider the opposite perspective. The only problem that could bring down the world's superpower, the United States, is debt. In this situation, could the U.S. stake its fate on a single new asset? For the stability of the reserve strategy, the U.S. might consider a hedging strategy of diversifying into multiple assets rather than relying on a single asset, which could be the only alternative to reduce systemic risk in the reserve system.

Additionally, although a minority opinion, Bitcoin is not a 100% trustworthy asset from the U.S. perspective. The identity of Satoshi Nakamoto remains unknown. There are suspicions that China might be behind it. This could pose an important risk from a national security perspective.

In this situation, Ripple can play an important role. Ripple can contribute to the U.S. strategy in two aspects.

First, from the perspective of multiple digital asset reserves. Ripple CEO Garlinghouse revealed on January 29 through his X (formerly Twitter) live that he had discussed with President Trump about introducing various digital assets including Ripple as U.S. strategic assets. Trump has already ordered the working group established through his January 23 executive order to submit a report within 180 days that includes an assessment of how to stockpile digital assets at the national level. These movements are interpreted as the Trump administration having already decided to stockpile multiple digital assets, not just Bitcoin, and building justification to implement this.

Ripple CEO Brad Garlinghouse and CLO Stuart Alderoty had dinner with President-elect Trump at the Mar-a-Lago Resort on January 7. (Source: X)

Second, in the role within a multiple reserve currency system. Currently, the dollar serves too many roles, including international trade settlement, store of value, and foreign exchange reserve asset, and must bear excessive debt to maintain these roles. Federal Reserve Chairman Jerome Powell has acknowledged this situation and mentioned the possibility of a multiple reserve currency system based on historical precedents.

Ripple can strategically share some of the dollar's roles. If Ripple replaces part of the dollar's role in international remittances and payments, the dollar can function more efficiently as a reserve currency.

Additionally, Ripple can play an important role in the CBDC era. Even if the United States doesn't directly issue a CBDC, it can maintain control of international finance in the CBDC era by connecting to other countries' CBDCs through Ripple's bridge role.

Above all, Ripple is an asset under U.S. control. Unlike Bitcoin, which is suspected of being dominated by China, Ripple is a system developed and operated by a U.S. company. This is an important advantage from a national security perspective.

A multi-asset reserve and multiple reserve currency strategy can be a practical solution to the problems facing the United States. Utilizing various digital assets rather than relying on a single asset is more effective for risk management, and a multiple reserve currency system can distribute the excessive burden currently borne by the dollar.

It remains to be seen what role Ripple will play in this process and how widely it will be adopted. But if we understand the essence of the problems facing the United States as a reserve currency nation, Ripple's adoption is certainly a possible scenario. Just as no one predicted the institutional adoption of Bitcoin ten years ago, but the appropriate technology emerged at the right time and rose to become the world's store of value, Ripple's prepared technology could satisfy the needs of the United States and the world at the appropriate time.

The world now stands on the verge of forming a new financial order. Although its exact shape is not yet clear, one certainty is that Ripple is highly likely to be at the center of that change. In the next chapter, we will examine in detail how Ripple is entering the stablecoin market and developing as a new investment vehicle through ETFs amidst these changes.